")

OUTLOOK FOR THE FINANCIAL MARKET AND OTHER IMPORTANT TOPICS FOR INVESTORS

A turning point in the markets

Inflation, high interest rates, risks of slower consumer spending, possibility of a US hard economic landing and increased geopolitical tensions are just some of the many issues that investors must currently deal with.

We have seen new worries come up in 2023 such as the prospect of a US default on its debt, concerns over the next US presidential election or the dysfunctional American congress that leads to uncertainty in the long-term funding of the budget of the United States .

We have witnessed many crises over the past years: pandemic, wars, political tensions, etc. From such experiences, investors know that the “market noise” can be quite loud, but that significant changes in prices do not necessarily reflect changes in the fundamental value of assets.

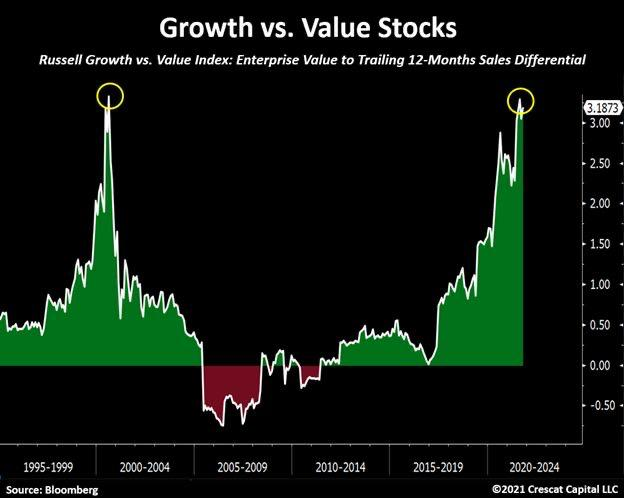

Investors have seen that market sentiment and paradigms change fast. We can remember that at the end of 2022, many analysts were negative on technology stocks, including Apple, Tesla, Amazon, Meta, Nvidia, Netflix orMicrosoft that have significantly outperformed indices in 2023.

We believe that corporations are telling the correct message when they are warning about slower consumer spending and an overall weaker economy. This should lead long-term interest rates to start to drop.

Considering that equity prices are more sensitive to interest rates than to earnings, we believe that the financial markets are now at a turning point, as in our viewlong-term bond yields have reached their peak.

In this this research note, we will discuss a variety of issues including inflation and interest rates. We will also quantify the upside on equity markets over the next 12 to 18 months.

We remain at your disposal for any questions and look forward to any comments or feedback from our distinguished Readers.

SUSSLAND & CO LTD.

1. Executive summary

- The key driver of the financial markets is the evolution of interest rates in the United States. 10-year US treasury yields are close to 5.00%. The last time that they were at these levels was in 2006 and 2007, before the financial crisis of 2008;

- Many US and European corporations are warning investors about a more difficult economic environment, highlighting weaker consumer spending;

- Despite these warnings from the private sector, central banks, including the US Fed, continue to declare that their principal worry is inflation;

- Investors are therefore worried that central banks are focusing on back-looking data rather than forward looking data. This could lead central banks to keep short-term interest rates at higher levels than necessary and for longer than necessary. Analysts fear that this could trigger a “hard” economic landing, or worse, a recession;

- The inflation that occurred after the pandemic was purely accidental. It would not have happened if there had not been multiple lockdowns in 2020 and 2021. The long-term trend for most of the world remains disinflation;

- Excess savings accumulated during the pandemic enabled consumer spending to remain strong in 2021 and 2022 despite high levels of inflation. However, the high level of interest rates is now clearly taking a toll on the ability of consumers to spend;

- Since consumers have a budget that is not extendable (wages have not increased as much as inflation or rents), these higher costs will require individuals to save on other areas. Over the past weeks we have seen companies warn over consumer weakness in many sectors including airline travel, toys, orthodontic products, cars, furniture, and restaurants.

- Analysts are therefore revising their revenues and earnings forecasts lower. Economists are also revising lower GDP growth in 2024;

- The natural consequence of lower growth, or possibly recession, is that long-term bond yields will drop. This drop will occur many months before central banks start to cut short-term interest rates in mid-2024:

- In our view, current stock prices fully price in lower expectations for 2024;

- Stock prices are much more sensitive to changes in interest rates than to changes in earnings. Historically, a 120bps drop in rates leads to an increase of the Nasdaq of 25%;

- We believe that the stock market has bottomed, and offers significant upside;

- Politics and geopolitics impact the markets in the short-term, but not in the long-term. Neither US politics, the war in Ukraine, the war in Israel, or China-US relations should affect the markets in the long run;

- With declining interest rates, bonds, equities, and gold should all see price increases;

- Our preferred equity sectors are technology, financials, consumer staples, and energy. In renewable energy, only solar energy appears to offer viable economics;

- In bonds, we advise investors to increase durations;

- The dollar will remain the reserve currency of the world and should appreciate due to high positive real interest rates. Talks about de-dollarization are unrealistic.

2. The current situation in the economy and the markets

2.1. Where are we coming from?

At the end of 2022, investor sentiment was extremely negative. In the United States, inflation was high, and analysts were expecting inflation to remain high and feared that interest rate increases by the US Fed would lead to an economic slowdown.

Contrary to expectations, the financial markets improved significantly over the first semester of 2023. This positive evolution followed the decline in inflation in the United States, which dropped from 6.5% in december 2022 to 3.0% in june 2023. Investors became more optimistic and started to expect the US central bank to become less restrictive.

However, since august 2023, the financial markets have been in a correction mode.

Several reasons can explain this.

First, at the end of july, many stocks became overbought, especially in technology where many stocks benefited from the excitement related to the opportunities arising from artificial intelligence (hereafter “AI”).

Second, the goodearnings for the second quarter of 2023 had been anticipated and were reflected in the share prices. There was not enough « new » news from companies to push stock prices higher.

Third, inflation in the United States started again to climb for reasons that will be discussed further, in section 3. The communication from the US Federal Reserve became increasingly hawkish (i.e., negative). Jerome Powell and other members of the Fed repeatedly indicatedthat inflation was not under control and that higher interest rates were necessary to bring inflation back below their long-term target of 2.00%.

It should be added that a) the US Fed did not change itsinflation target and b) the US Fed has stated that it wants to reach its inflation target as fast as possible. The financial markets, which had been previously expecting that the first interest cuts would occur in early 2024, now onlyexpect the first interest rate cuts in july 2024.

2.2. Where are we now?

While at the beginning of the year, the economic base case was the one of a “soft landing”, i.e., a gradual slowdown in the economy, economists are now more and more worried about a “harder” economic landing.

Indeed, high interest rates are posing an increasing risk for economic growth.