")

This is not a recommendation but just our opinion. Please consult with your financial advisor before investing!

What style to favor? Value or growth? Or both?

Investors often classify stocks into two categories: value or growth.

The first category includes traditional companies, with stocks that have fairly reasonable valuations and often pay high dividends. Companies are generally well-established and are active in "relatively" stable and predictable industries. Managers are often experienced people with many years of experience.

The second category is made up of rather young, high-growth companies, often with high valuations, driven by investors' hopes of seeing revenues and profits increase sharply in the future. These companies are often in new markets (often technology or biotechnology) where the risks of disruption and competition are remarkably high, and where the visibility of future revenues is not always clear.

Depending on the economic context and the period, these two categories of securities may evolve in a similar way or differently when investors have a marked preference for one or the other of these categories.

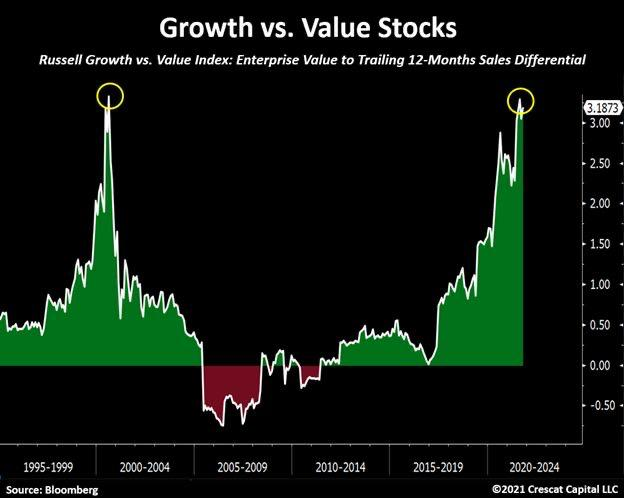

Unsurprisingly, over the past five years, growth stocks have largely outperformed value stocks. In percentage terms, the difference is 60.48% and the gap between the two categories has never been greater. In a world in which growth is almost non-existent, marked by the trade war, Brexit, Covid-19 and other geopolitical tensions, technology and healthcare stocks seem to be among the few that are able to increase their revenues.

However, all things come to an end, and when the craze for techno will subdue, there may be some nasty stock market surprises. In fact, the progression of many stocks is more related to the expansion of valuation multiples than to revenue or earnings growth alone. For example, Apple's P/E ratio has risen from 15x in 2018 to 30x today. In other words, investors are paying twice as much for Apple's earnings today as they were two years ago. In the case of Microsoft, the P/E ratio has increased in two years from 25x to more than 32x. In the case of Tesla, from 48x in early 2019 to over 311x today. Tesla's capitalization today represents 60% of the capitalization of Warren Buffet's conglomerate, while Tesla's earnings represent only 5% of those expected from Berkshire Hathaway.

In short, in a world in lockdown due to covid-19, most technology stocks have undergone a significant revaluation with investors paying more and more for growth. Valuations are becoming strained. A small grain of sand could make the machine stall. Politicians on both sides of the Atlantic are talking more and more about regulating social networks, taxing internet corporate profits differently and, in some cases, splitting into several pieces some of the largest companies with overly dominant market shares.

Growth comes at a price, caveat emptor.

Do not hesitate to contact us !

Contact us