Since the late 1970s and early 1980s, many developed countries have not experienced inflation. To the contrary, inflation rates have kept falling, dragging interest rates lower.

Forty years of disinflation

This phenomenon of "disinflation" can be explained by three factors.

The first factor is the demographic trend marked by a drop in the number of births. Indeed, the strong increase in the population after the Second World War (“baby boom”) has given way to a sharp decrease in fertility. This is explained by the increase in the percentage of women in the workforce, the rise in unemployment and lower economic growth which makes the financial situation of households more precarious, as well as the high costs related to children (childcare, education, health).

The second is linked to the development of the service sector, which is less impacted by variations in the cost of raw materials.

The third factor is related to new technologies, especially information technology (IT), which is highly deflationary by nature. For example, many trade unions are concerned about the increased use of robots that end up replacing humans for increasingly complex tasks. Robots can be up to fifty times cheaper than humans and they can work 24 hours a day, seven days a week.

Please find hereafter some brief comments on this event.

Note that we do not yet know all the details surrounding the events at the time of this writing.

OUTLOOK FOR THE FINANCIAL MARKET AND OTHER IMPORTANT TOPICS FOR INVESTORS Dear Reader, Each new year is an opportunity to perform a new assessment of the world's economic and political situation, to evaluate what could stay the same and what could change, and try to identify risks and opportunities in the financial markets As we…

OUTLOOK FOR THE FINANCIAL MARKET AND OTHER IMPORTANT TOPICS FOR INVESTORS A turning point in the markets Inflation, high interest rates, risks of slower consumer spending, possibility of a US hard economic landing and increased geopolitical tensions are just some of the many issues that investors must currently deal with. We have seen new worries…

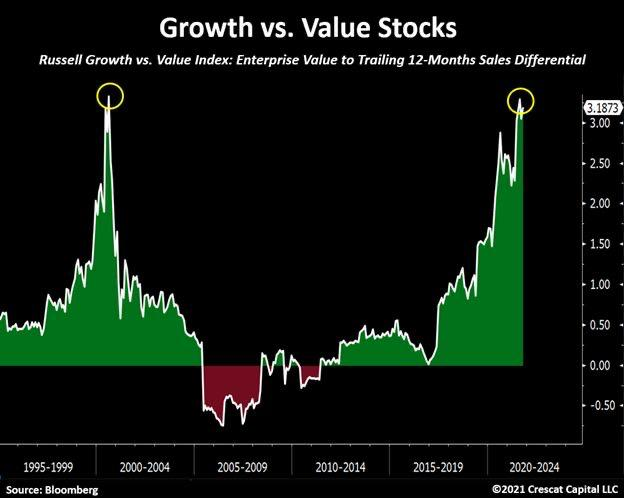

Investors often distinguish between high growth companies ("growth stocks") and defensive companies ("value shares"). The purpose of this distinction is to take into account the expected future growth in the frame of the valuation of the share price. Indeed, this is the only realistic way to compare a growing company with a company whose business…

")